Resources: Blog Articles and Videos

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Welcome to our Resource Center

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

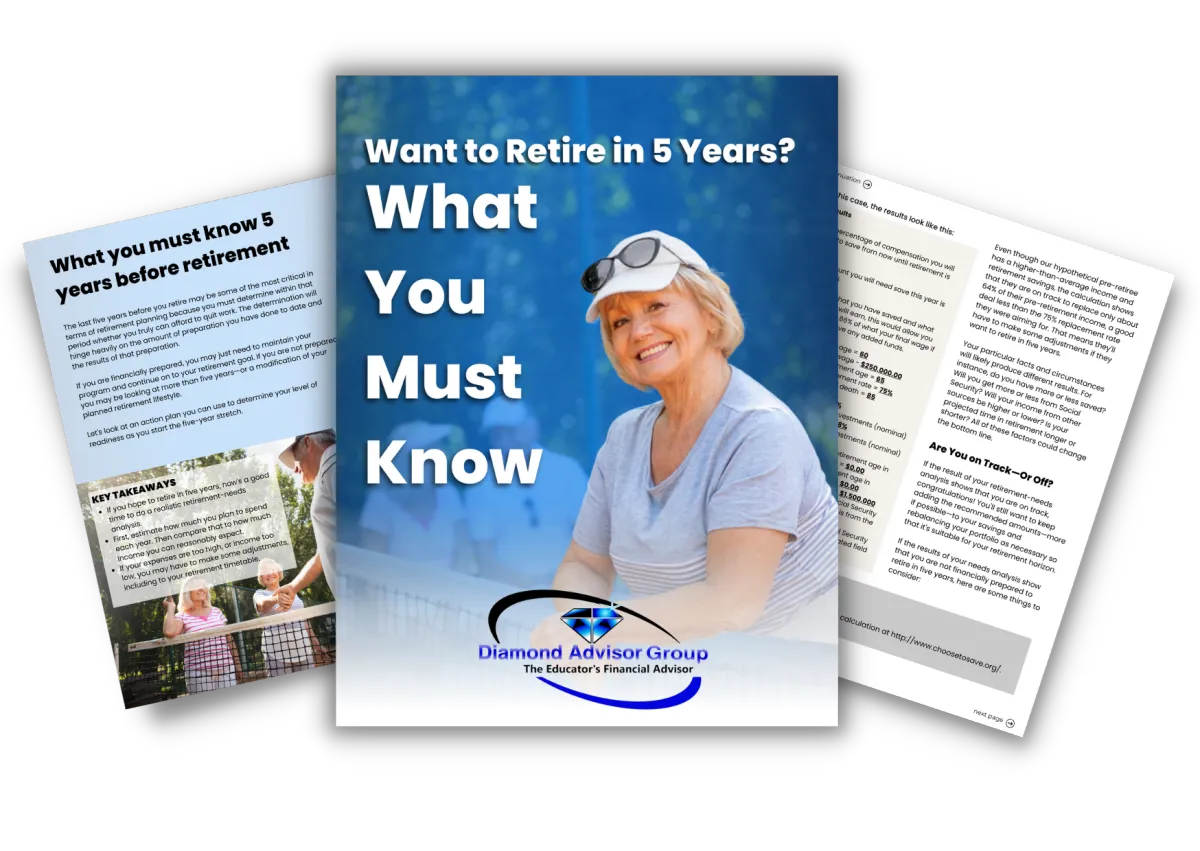

What You Must Know 5 Years Before Retirement

May 04, 2022

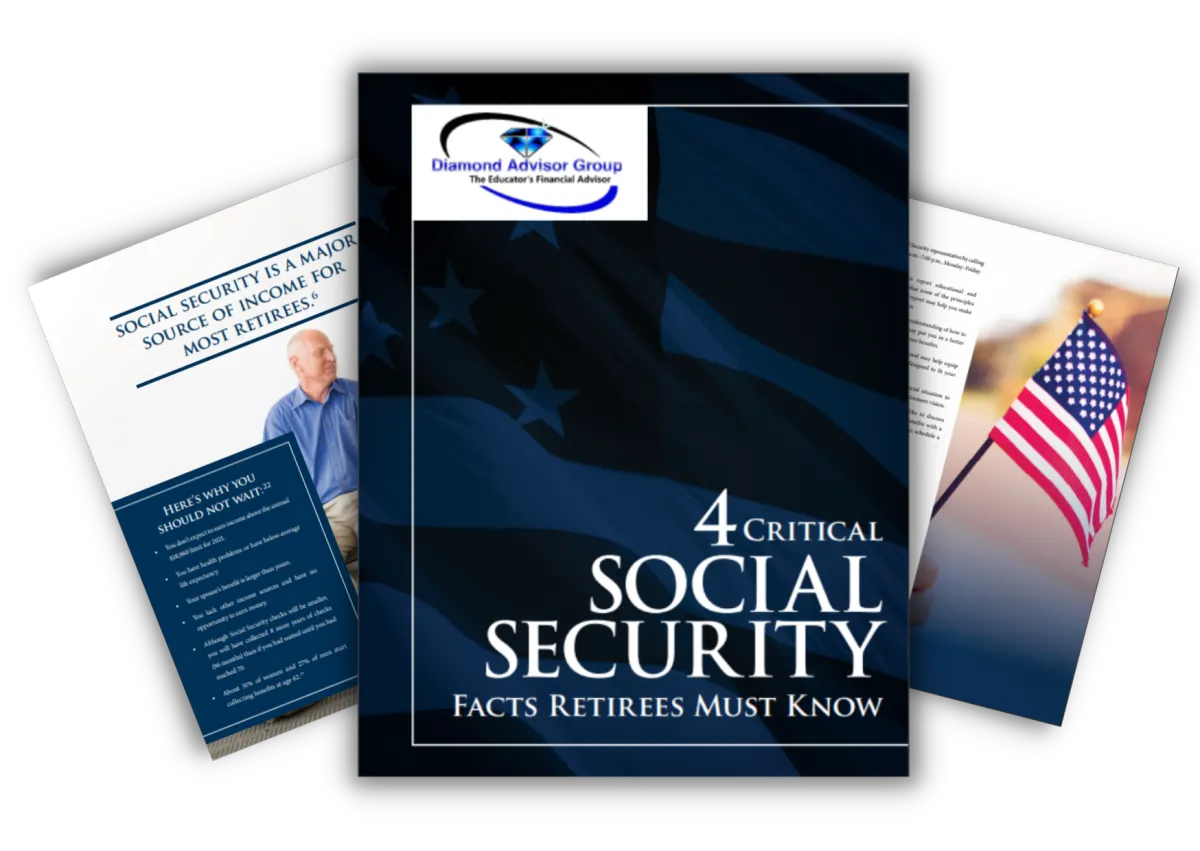

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

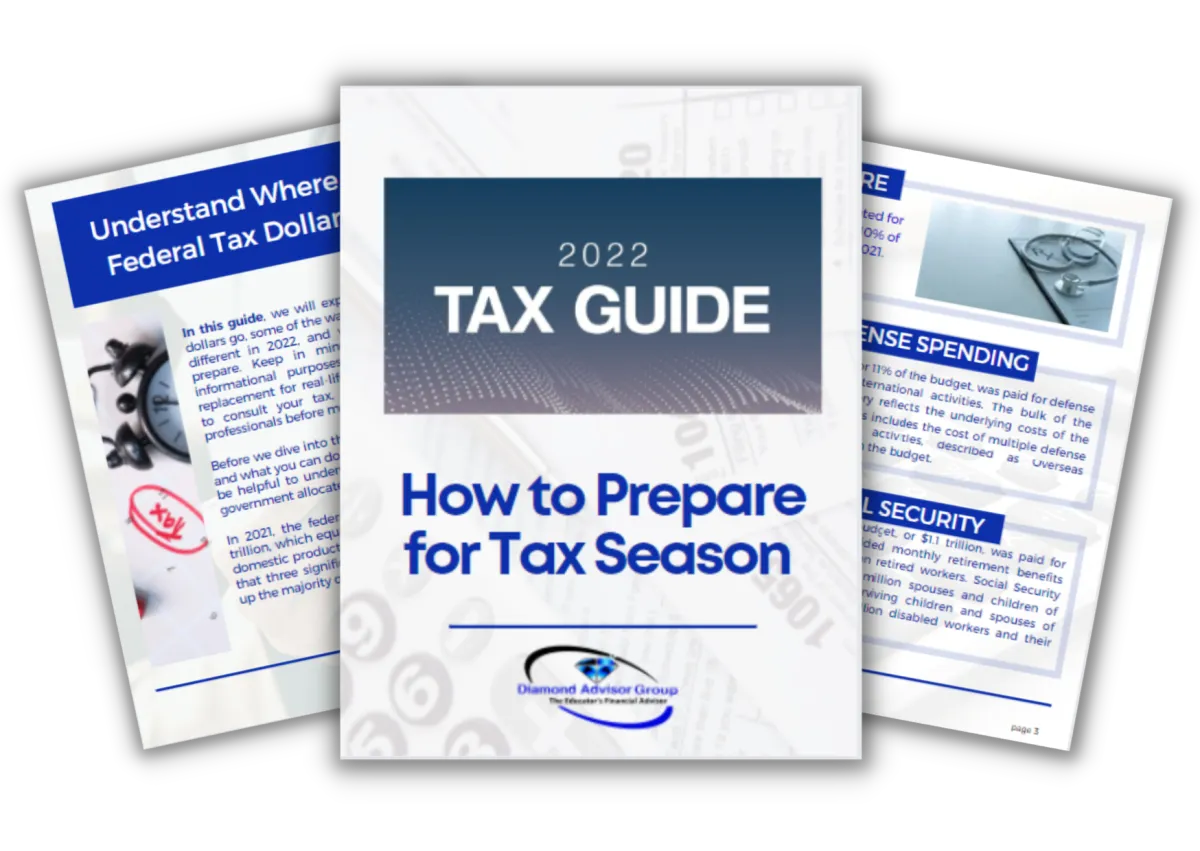

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Are North Carolina TEACHERS Unwittingly Handing Over Their Retirement?

Are North Carolina TEACHERS Unwittingly Handing Over Their Retirement?

Most North Carolina teachers assume that TSERS—the Teachers' and State Employees’ Retirement System—handles everything automatically. You contribute, the system grows, and one day you get your pension.

But here’s the truth many teachers discover too late:

👉 TSERS gives you benefits… but not control.

Why TSERS Isn’t the Whole Story

Yes, TSERS provides a guaranteed pension.

But it also brings limitations:

• You don’t choose the investments.

• You can’t adjust the plan to fit your goals.

• And most importantly… TSERS won’t update your beneficiary for you.

That last part? It’s a silent trap.

The Risk Teachers Don’t See Coming

Life changes—marriage, divorce, kids—and your TSERS beneficiary form doesn’t follow along. If it’s out of date, your pension might go to the wrong person.

It happens more often than most teachers think.

How Teachers Can Take Back Control

This is where supplemental accounts like 403(b)s and 457 plans come in. They offer:

✔️ Investment control

✔️ Contribution flexibility

✔️ Long-term growth

✔️ Easy beneficiary updates

You’re no longer relying on one system—you’re building a retirement plan around your life.

A Real Example

A North Carolina teacher came to me after 18 years in the classroom. She assumed everything was set—until we discovered her ex-partner was still listed on her TSERS paperwork.

We fixed it in minutes.

Then she opened a 457 plan and started contributing a small amount monthly. Over time, those contributions grew into a six-figure account that she fully controlled.

One review. One decision. Total peace of mind.

Watch the Full Breakdown

If you missed the Retirement Ready live session on this topic, you can watch the full replay here:

👉 Watch the Replay on YouTube

Final Thoughts

TSERS is a powerful tool—but it shouldn’t be your only strategy. When teachers add supplemental accounts and keep beneficiaries updated, they regain control over their future.

Your retirement shouldn’t be left to chance. And with a few simple steps, it won’t be.

📌 Next Step:

Let’s take a closer look at your retirement plan together.

👉https://bit.ly/4440F9l

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

What You Must Know 5 Years Before Retirement

May 04, 2022

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Are North Carolina TEACHERS Unwittingly Handing Over Their Retirement?

Are North Carolina TEACHERS Unwittingly Handing Over Their Retirement?

Most North Carolina teachers assume that TSERS—the Teachers' and State Employees’ Retirement System—handles everything automatically. You contribute, the system grows, and one day you get your pension.

But here’s the truth many teachers discover too late:

👉 TSERS gives you benefits… but not control.

Why TSERS Isn’t the Whole Story

Yes, TSERS provides a guaranteed pension.

But it also brings limitations:

• You don’t choose the investments.

• You can’t adjust the plan to fit your goals.

• And most importantly… TSERS won’t update your beneficiary for you.

That last part? It’s a silent trap.

The Risk Teachers Don’t See Coming

Life changes—marriage, divorce, kids—and your TSERS beneficiary form doesn’t follow along. If it’s out of date, your pension might go to the wrong person.

It happens more often than most teachers think.

How Teachers Can Take Back Control

This is where supplemental accounts like 403(b)s and 457 plans come in. They offer:

✔️ Investment control

✔️ Contribution flexibility

✔️ Long-term growth

✔️ Easy beneficiary updates

You’re no longer relying on one system—you’re building a retirement plan around your life.

A Real Example

A North Carolina teacher came to me after 18 years in the classroom. She assumed everything was set—until we discovered her ex-partner was still listed on her TSERS paperwork.

We fixed it in minutes.

Then she opened a 457 plan and started contributing a small amount monthly. Over time, those contributions grew into a six-figure account that she fully controlled.

One review. One decision. Total peace of mind.

Watch the Full Breakdown

If you missed the Retirement Ready live session on this topic, you can watch the full replay here:

👉 Watch the Replay on YouTube

Final Thoughts

TSERS is a powerful tool—but it shouldn’t be your only strategy. When teachers add supplemental accounts and keep beneficiaries updated, they regain control over their future.

Your retirement shouldn’t be left to chance. And with a few simple steps, it won’t be.

📌 Next Step:

Let’s take a closer look at your retirement plan together.

👉https://bit.ly/4440F9l

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Hear From Our Clients

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

© 2022 Diamond Advisor Group - All Rights Reserved

Disclaimer