Resources: Blog Articles and Videos

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Welcome to our Resource Center

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

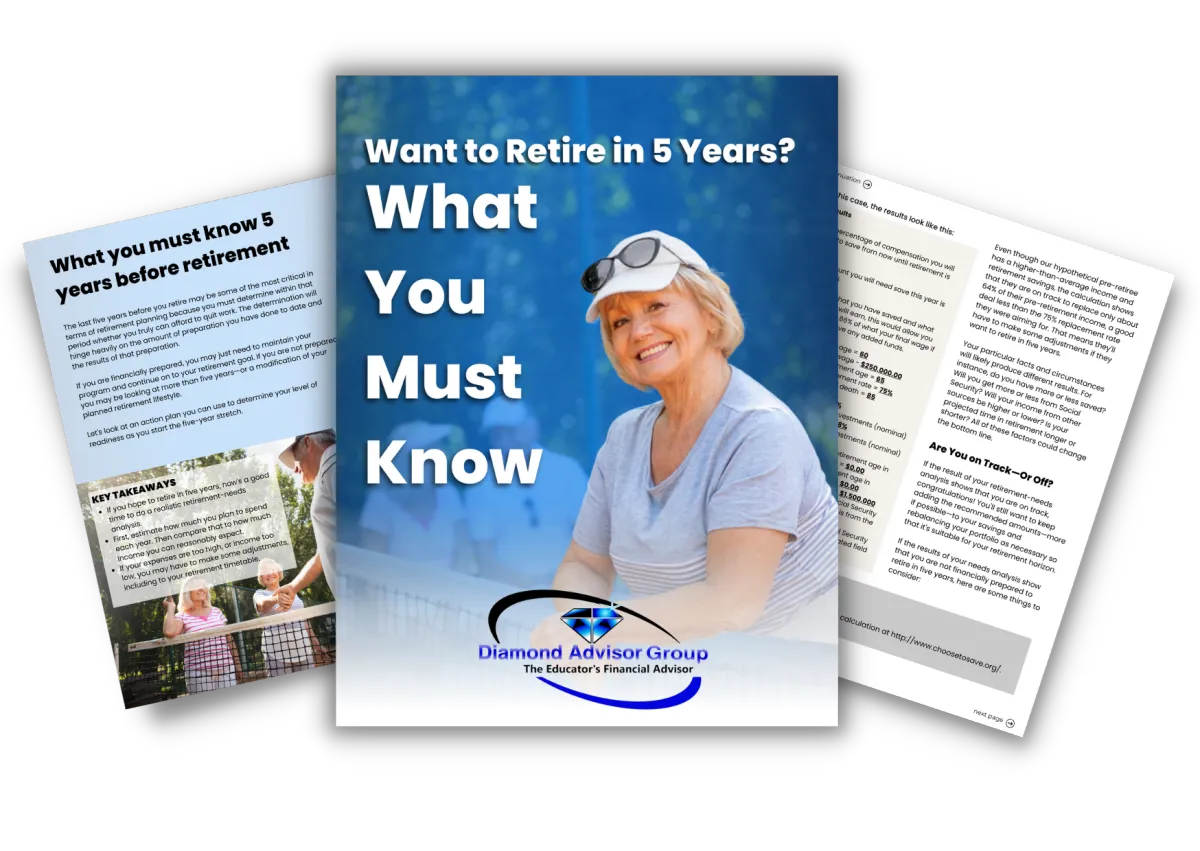

What You Must Know 5 Years Before Retirement

May 04, 2022

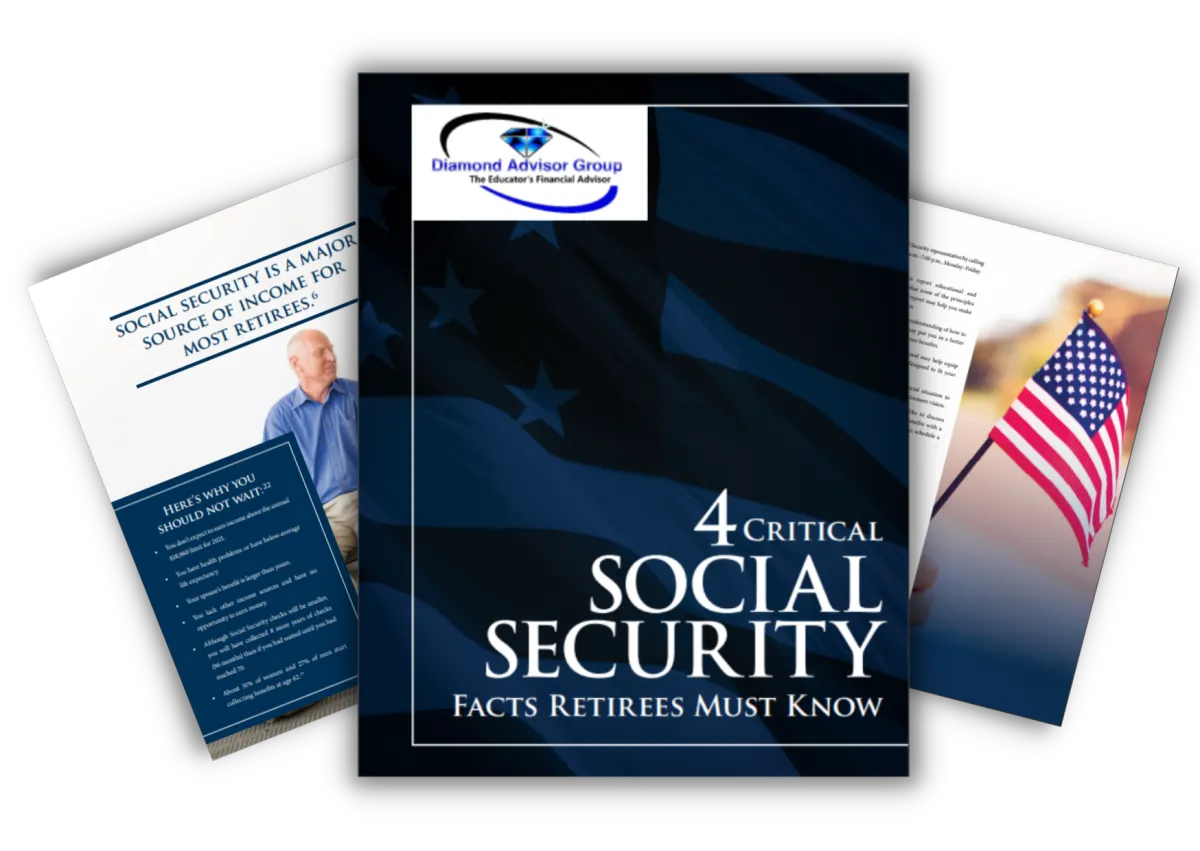

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

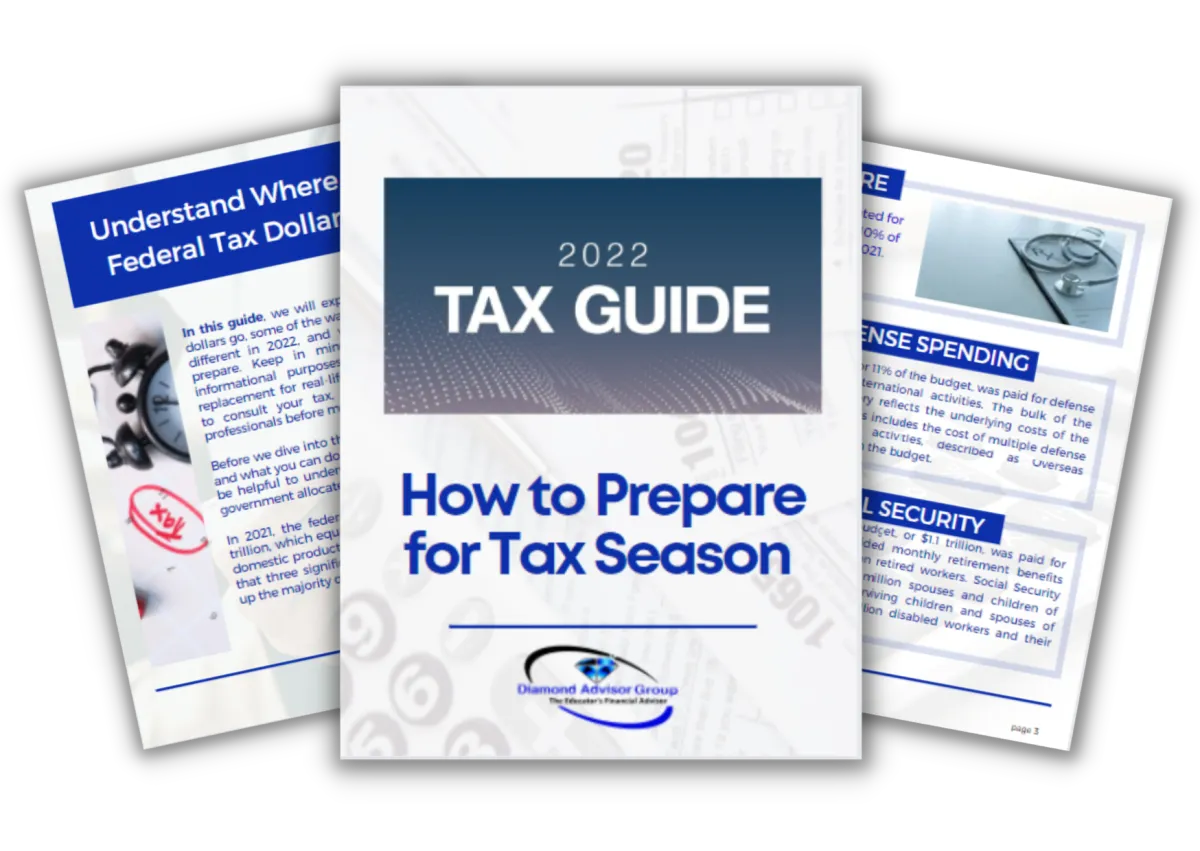

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

The Unseen Roadblock: How the Windfall Elimination Provision (WEP) Affects North Carolina Teachers' Social Security Benefits

The Unseen Roadblock: How the Windfall Elimination Provision (WEP) Affects North Carolina Teachers' Social Security Benefits

The Windfall Elimination Provision (WEP) is a significant, often misunderstood, factor that affects the retirement plans of North Carolina teachers. Many teachers in the state receive pensions through the Teachers' and State Employees' Retirement System (TSERS), which does not require them to pay into Social Security during their teaching careers. However, teachers who have worked in other jobs, where they did contribute to Social Security, often find themselves surprised when WEP reduces the benefits they thought they’d receive.

So, how does WEP work? Normally, Social Security benefits are calculated based on your average monthly earnings over the years. For most workers, the formula allows for 90% of the first segment of their earnings to count towards their benefits. However, when WEP applies, that percentage can drop as low as 40%, depending on how many years you've worked in Social Security-covered jobs.

This reduction can lead to a substantial loss. In 2024, for example, the maximum monthly reduction caused by WEP is $557.50. That’s over $6,500 per year—a significant amount for a retiree who’s relying on both a pension and Social Security to make ends meet.

For North Carolina teachers, the situation can feel like a double-edged sword. They’ve spent years serving the community through their work in education, but because they didn’t contribute to Social Security while teaching, they now face reduced benefits. Many teachers also worked summer jobs, part-time positions, or even second careers after retiring from the classroom, paying into Social Security with those earnings, only to find that WEP slashes the expected payout.

But what can be done? The good news is that teachers can take steps to reduce the impact of WEP. One strategy is to continue working in Social Security-covered employment for at least 30 years. If you have 30 years of substantial earnings in such jobs, WEP will no longer apply to you. Even if you have between 20 and 30 years, the reduction caused by WEP will be smaller.

It’s also important to focus on maximizing your TSERS pension. By staying in the system longer or considering service purchase options, you can increase your pension payouts, which may help offset any Social Security losses due to WEP.

Lastly, working with a financial advisor can provide personalized strategies for planning a secure retirement. They can help you calculate your expected retirement income and navigate complex issues like WEP, ensuring you’re not caught off guard when the time comes.

Are you concerned about how WEP could impact your retirement? Book a free 15-minute Zoom call to discuss how to protect your Social Security benefits and create a more secure retirement plan!

Click here to book a call 👉https://learn.dondaves.net/webinar-2616

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

What You Must Know 5 Years Before Retirement

May 04, 2022

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

The Unseen Roadblock: How the Windfall Elimination Provision (WEP) Affects North Carolina Teachers' Social Security Benefits

The Unseen Roadblock: How the Windfall Elimination Provision (WEP) Affects North Carolina Teachers' Social Security Benefits

The Windfall Elimination Provision (WEP) is a significant, often misunderstood, factor that affects the retirement plans of North Carolina teachers. Many teachers in the state receive pensions through the Teachers' and State Employees' Retirement System (TSERS), which does not require them to pay into Social Security during their teaching careers. However, teachers who have worked in other jobs, where they did contribute to Social Security, often find themselves surprised when WEP reduces the benefits they thought they’d receive.

So, how does WEP work? Normally, Social Security benefits are calculated based on your average monthly earnings over the years. For most workers, the formula allows for 90% of the first segment of their earnings to count towards their benefits. However, when WEP applies, that percentage can drop as low as 40%, depending on how many years you've worked in Social Security-covered jobs.

This reduction can lead to a substantial loss. In 2024, for example, the maximum monthly reduction caused by WEP is $557.50. That’s over $6,500 per year—a significant amount for a retiree who’s relying on both a pension and Social Security to make ends meet.

For North Carolina teachers, the situation can feel like a double-edged sword. They’ve spent years serving the community through their work in education, but because they didn’t contribute to Social Security while teaching, they now face reduced benefits. Many teachers also worked summer jobs, part-time positions, or even second careers after retiring from the classroom, paying into Social Security with those earnings, only to find that WEP slashes the expected payout.

But what can be done? The good news is that teachers can take steps to reduce the impact of WEP. One strategy is to continue working in Social Security-covered employment for at least 30 years. If you have 30 years of substantial earnings in such jobs, WEP will no longer apply to you. Even if you have between 20 and 30 years, the reduction caused by WEP will be smaller.

It’s also important to focus on maximizing your TSERS pension. By staying in the system longer or considering service purchase options, you can increase your pension payouts, which may help offset any Social Security losses due to WEP.

Lastly, working with a financial advisor can provide personalized strategies for planning a secure retirement. They can help you calculate your expected retirement income and navigate complex issues like WEP, ensuring you’re not caught off guard when the time comes.

Are you concerned about how WEP could impact your retirement? Book a free 15-minute Zoom call to discuss how to protect your Social Security benefits and create a more secure retirement plan!

Click here to book a call 👉https://learn.dondaves.net/webinar-2616

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Hear From Our Clients

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

© 2022 Diamond Advisor Group - All Rights Reserved

Disclaimer