Resources: Blog Articles and Videos

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Welcome to our Resource Center

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

What You Must Know 5 Years Before Retirement

May 04, 2022

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

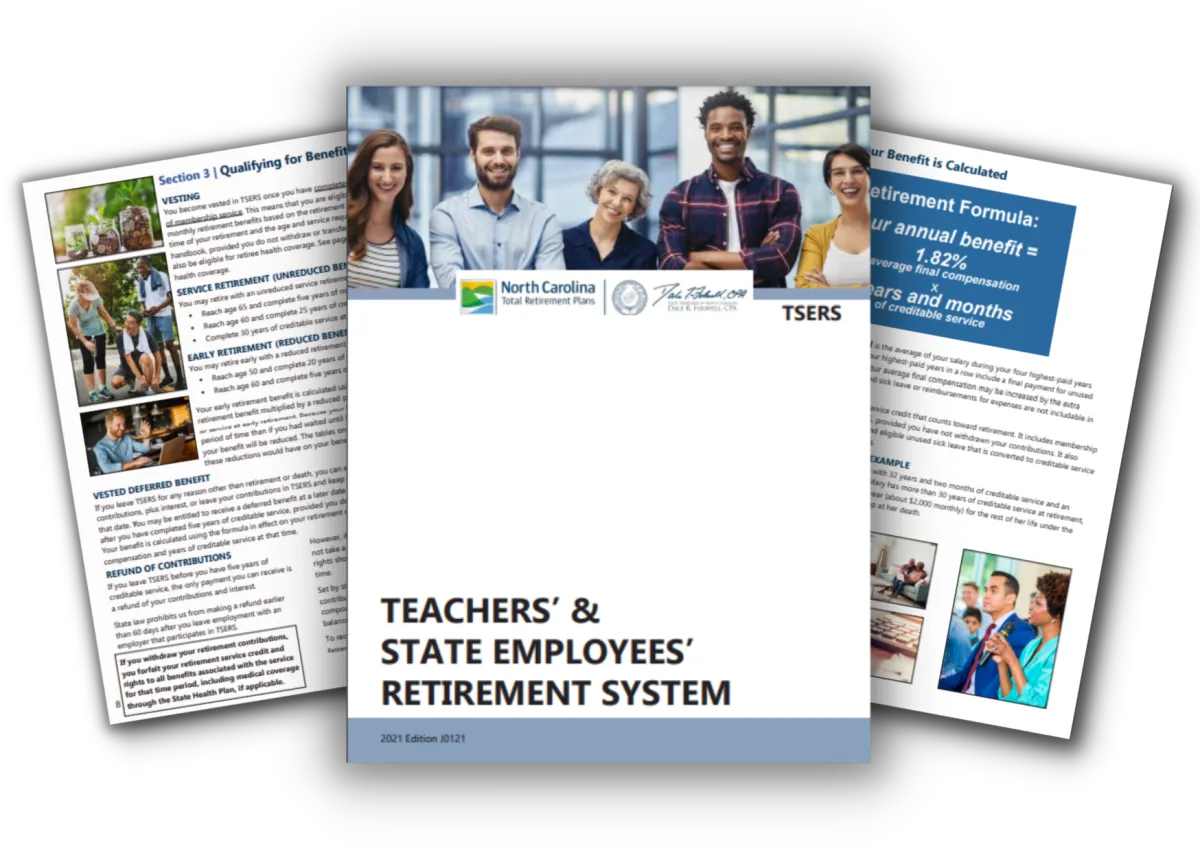

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Will Your Retirement Savings Last Until 100? NC Teachers, Here’s the Truth!

Will Your Retirement Savings Last Until 100? NC Teachers, Here’s the Truth!

The Harsh Reality of Retiring at 65

Imagine this: You’ve worked tirelessly for decades, shaping young minds, grading papers late into the night, attending endless meetings, and now, finally—it’s time to retire! But here’s the question no one wants to ask: Will your money last as long as you do?

With rising costs, longer life expectancies, and unpredictable market conditions, many retirees—especially teachers—find themselves in financial trouble just when they need stability the most. The good news? You can take control of your financial future right now.

Why NC Teachers Need a Different Retirement Plan

Most North Carolina teachers rely heavily on their pension. While it’s a fantastic benefit, it may not be enough to cover a 30+ year retirement. Here’s why:

Inflation is a silent thief. A pension that seems comfortable today may not stretch as far in 20 years.

Healthcare costs are rising. Medicare doesn’t cover everything, and long-term care can drain your savings fast.

People are living longer. If you retire at 65 and live to 95 or even 100, that’s 35 years of expenses you need to plan for!

Social Security alone isn’t enough. The average Social Security payout won’t cover your current standard of living.

So, what’s the plan? Let’s break it down.

How to Know If Your Savings Will Last

First, let’s do some quick math (don’t worry, I’ll keep it simple!). Ask yourself:

How much do you currently have saved? Include your pension, 401(k), IRAs, and any personal savings.

How much do you expect to spend each year in retirement? Housing, healthcare, travel, and everyday living expenses all add up.

How long do you expect to live? While none of us have a crystal ball, planning for 90-100 years old is a safe bet.

A common rule of thumb is the 4% withdrawal rule, meaning you should be able to withdraw 4% of your savings each year and have it last for 30 years. But if you’re retiring earlier or living longer, you may need to adjust that number!

The Biggest Retirement Risks NC Teachers Face

1. Underestimating Healthcare Costs

Long-term care, prescriptions, and out-of-pocket expenses can skyrocket.

A solid strategy: Look into a Health Savings Account (HSA) and long-term care insurance.

2. Not Adjusting for Inflation

If inflation averages 3%, your purchasing power will cut in half in about 24 years.

A solid strategy: Invest in assets that grow over time, like real estate or a diversified stock portfolio.

3. Relying Too Heavily on Your Pension

While stable, pensions don’t always keep up with inflation or unexpected costs.

A solid strategy: Supplement with personal savings, side income, or annuities.

Smart Moves to Secure Your Retirement

Ready to take control? Here are three powerful steps you can take today:

1. Maximize Your Pension Benefits

Understand your payout options (lump sum vs. monthly benefits).

Know your survivor benefits to protect your spouse.

2. Boost Your Savings with a 403(b) or IRA

These accounts help you grow tax-advantaged savings.

Even small monthly contributions now can make a big difference later!

3. Create Multiple Streams of Income

Consider part-time work, rental properties, or passive investments.

More income = Less stress about outliving your savings!

FAQs: Your Retirement Questions, Answered!

Q: What if I don’t have enough saved yet?

A: It’s never too late! Increase savings, lower expenses, and explore investment options. Small changes add up!

Q: How can I make my pension stretch further?

A: Budget wisely, delay Social Security to maximize benefits, and avoid unnecessary withdrawals from savings.

Q: Should I keep working part-time in retirement?

A: If you enjoy it, yes! Even a small side income can help reduce financial stress and keep you active.

Final Thoughts: Take Action Today

Your retirement should be a time of freedom, not financial fear. Whether you’re retiring soon or years away, the best time to plan is NOW.

🔹 Review your savings. Know where you stand. 🔹 Make a plan. Adjust for inflation, healthcare, and longevity. 🔹 Take action. The sooner you start, the stronger your future will be!

📅 Ready to take the next step? Book your appointment today: https://bit.ly/4440F9l

💬 Have questions or want to dive deeper? Let’s connect!

💼 LinkedIn: https://www.linkedin.com/in/don-daves/

📘 Facebook: https://www.facebook.com/diamondadvisorgrp

Youtube: https://www.youtube.com/@diamondgroup4496/playlists

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

What You Must Know 5 Years Before Retirement

May 04, 2022

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Will Your Retirement Savings Last Until 100? NC Teachers, Here’s the Truth!

Will Your Retirement Savings Last Until 100? NC Teachers, Here’s the Truth!

The Harsh Reality of Retiring at 65

Imagine this: You’ve worked tirelessly for decades, shaping young minds, grading papers late into the night, attending endless meetings, and now, finally—it’s time to retire! But here’s the question no one wants to ask: Will your money last as long as you do?

With rising costs, longer life expectancies, and unpredictable market conditions, many retirees—especially teachers—find themselves in financial trouble just when they need stability the most. The good news? You can take control of your financial future right now.

Why NC Teachers Need a Different Retirement Plan

Most North Carolina teachers rely heavily on their pension. While it’s a fantastic benefit, it may not be enough to cover a 30+ year retirement. Here’s why:

Inflation is a silent thief. A pension that seems comfortable today may not stretch as far in 20 years.

Healthcare costs are rising. Medicare doesn’t cover everything, and long-term care can drain your savings fast.

People are living longer. If you retire at 65 and live to 95 or even 100, that’s 35 years of expenses you need to plan for!

Social Security alone isn’t enough. The average Social Security payout won’t cover your current standard of living.

So, what’s the plan? Let’s break it down.

How to Know If Your Savings Will Last

First, let’s do some quick math (don’t worry, I’ll keep it simple!). Ask yourself:

How much do you currently have saved? Include your pension, 401(k), IRAs, and any personal savings.

How much do you expect to spend each year in retirement? Housing, healthcare, travel, and everyday living expenses all add up.

How long do you expect to live? While none of us have a crystal ball, planning for 90-100 years old is a safe bet.

A common rule of thumb is the 4% withdrawal rule, meaning you should be able to withdraw 4% of your savings each year and have it last for 30 years. But if you’re retiring earlier or living longer, you may need to adjust that number!

The Biggest Retirement Risks NC Teachers Face

1. Underestimating Healthcare Costs

Long-term care, prescriptions, and out-of-pocket expenses can skyrocket.

A solid strategy: Look into a Health Savings Account (HSA) and long-term care insurance.

2. Not Adjusting for Inflation

If inflation averages 3%, your purchasing power will cut in half in about 24 years.

A solid strategy: Invest in assets that grow over time, like real estate or a diversified stock portfolio.

3. Relying Too Heavily on Your Pension

While stable, pensions don’t always keep up with inflation or unexpected costs.

A solid strategy: Supplement with personal savings, side income, or annuities.

Smart Moves to Secure Your Retirement

Ready to take control? Here are three powerful steps you can take today:

1. Maximize Your Pension Benefits

Understand your payout options (lump sum vs. monthly benefits).

Know your survivor benefits to protect your spouse.

2. Boost Your Savings with a 403(b) or IRA

These accounts help you grow tax-advantaged savings.

Even small monthly contributions now can make a big difference later!

3. Create Multiple Streams of Income

Consider part-time work, rental properties, or passive investments.

More income = Less stress about outliving your savings!

FAQs: Your Retirement Questions, Answered!

Q: What if I don’t have enough saved yet?

A: It’s never too late! Increase savings, lower expenses, and explore investment options. Small changes add up!

Q: How can I make my pension stretch further?

A: Budget wisely, delay Social Security to maximize benefits, and avoid unnecessary withdrawals from savings.

Q: Should I keep working part-time in retirement?

A: If you enjoy it, yes! Even a small side income can help reduce financial stress and keep you active.

Final Thoughts: Take Action Today

Your retirement should be a time of freedom, not financial fear. Whether you’re retiring soon or years away, the best time to plan is NOW.

🔹 Review your savings. Know where you stand. 🔹 Make a plan. Adjust for inflation, healthcare, and longevity. 🔹 Take action. The sooner you start, the stronger your future will be!

📅 Ready to take the next step? Book your appointment today: https://bit.ly/4440F9l

💬 Have questions or want to dive deeper? Let’s connect!

💼 LinkedIn: https://www.linkedin.com/in/don-daves/

📘 Facebook: https://www.facebook.com/diamondadvisorgrp

Youtube: https://www.youtube.com/@diamondgroup4496/playlists

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Hear From Our Clients

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

© 2022 Diamond Advisor Group - All Rights Reserved

Disclaimer