Resources: Blog Articles and Videos

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Welcome to our Resource Center

We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and

other financial concepts that will help you in planning for your future.

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

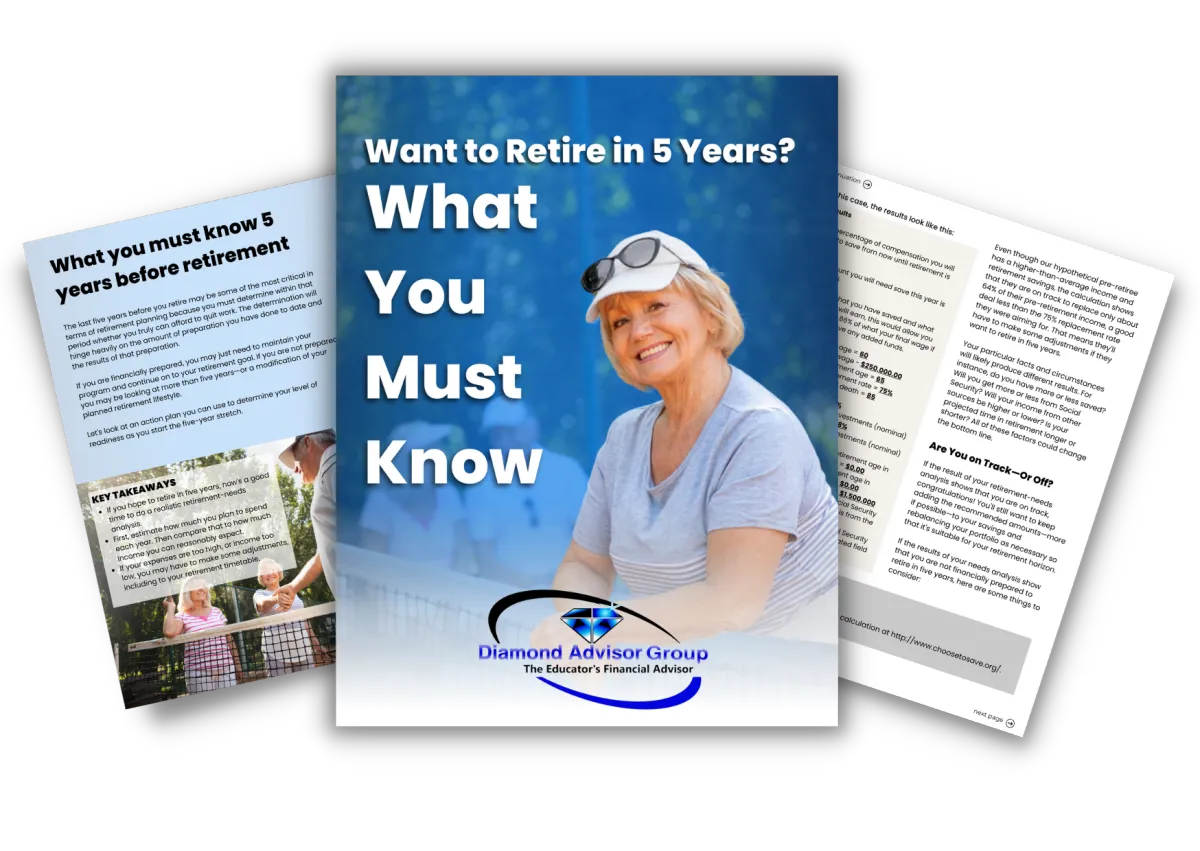

What You Must Know 5 Years Before Retirement

May 04, 2022

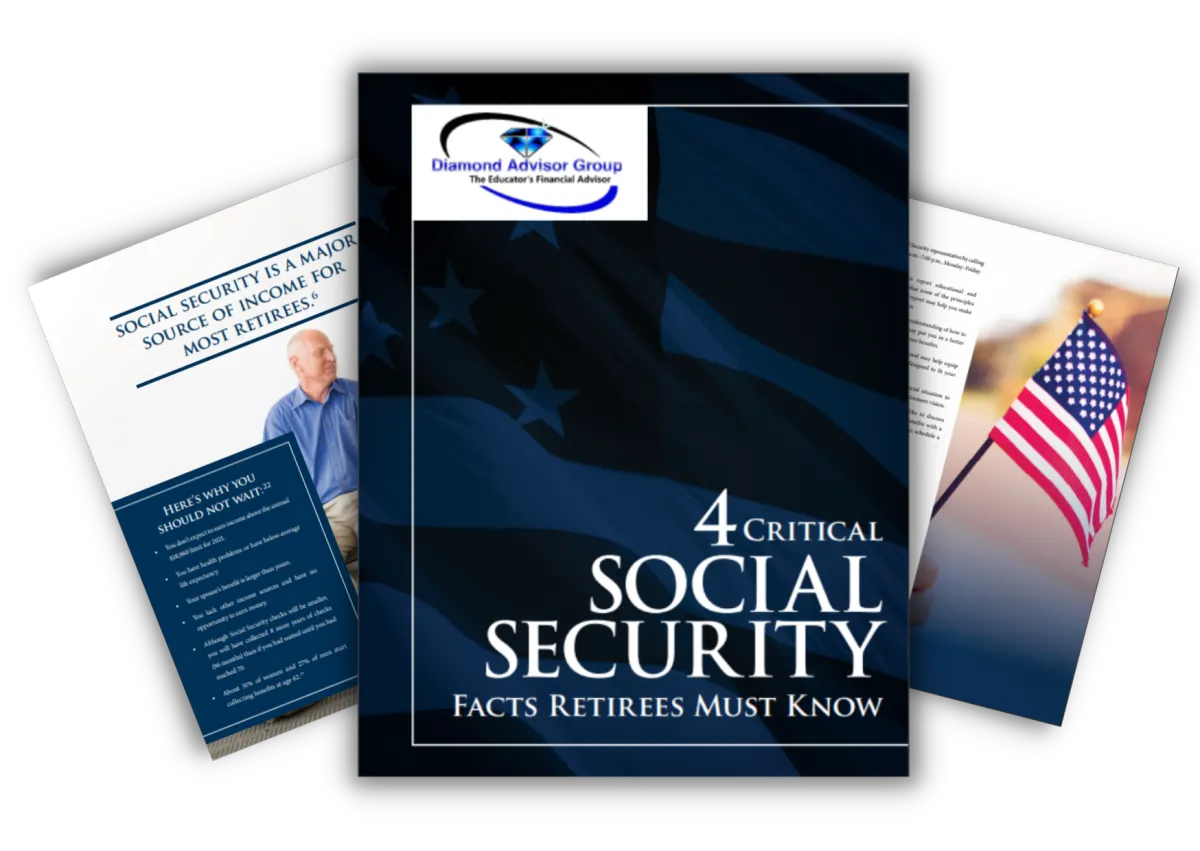

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

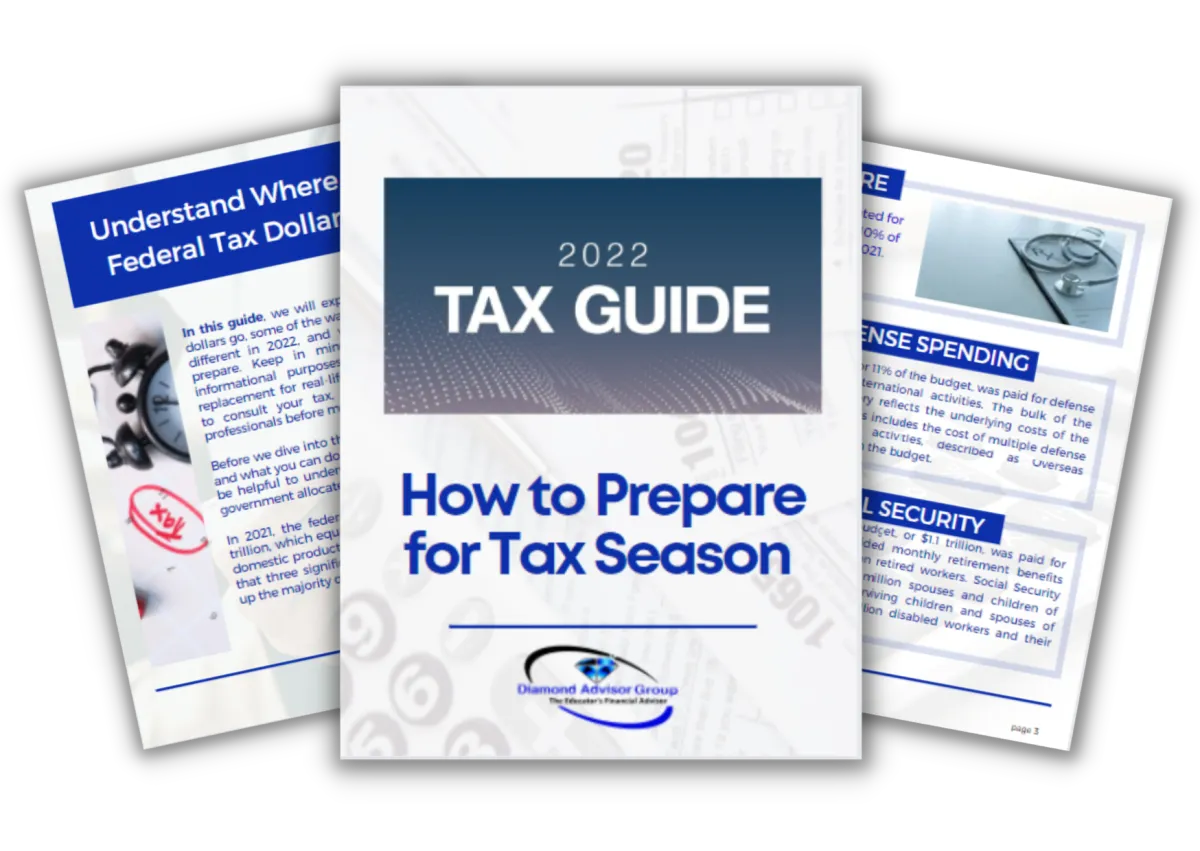

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Is Long-Term Care WIPING OUT Your Savings?

Is Long-Term Care WIPING OUT Your Savings?

What Every NC Teacher Needs to Know

Picture this: You’ve spent decades in the classroom, shaping young minds, grading endless stacks of papers, and finally—finally—you’re ready to retire. Your pension and savings should cover you, right? But then, an unexpected health issue pops up. A sudden need for long-term care, and before you know it, your nest egg is vanishing faster than you ever imagined.

This is the retirement nightmare that too many teachers face. The good news? You can take action NOW to protect your financial future. Let’s break down the real cost of long-term care and, more importantly, what you can do to keep your savings intact.

The Hidden Cost of Long-Term Care

Many people assume that Medicare will cover all their healthcare expenses in retirement. Spoiler alert: It won’t. Medicare provides only limited coverage for long-term care, leaving many retirees scrambling to pay for essential services like assisted living, nursing homes, or home health aides.

The Numbers Don’t Lie

Let’s talk real numbers. According to Genworth’s 2023 Cost of Care Survey, the average costs in North Carolina are:

In-home care: $4,900/month

Assisted living facility: $4,250/month

Nursing home (private room): $8,200/month

Multiply that by a few years, and you could be looking at a six-figure bill—and that’s without considering rising healthcare inflation!

Why NC Teachers Are Especially at Risk

North Carolina teachers have a solid pension, but let’s be honest—it’s not designed to cover massive healthcare expenses. Most teachers don’t have access to employer-sponsored retiree health benefits, and if you’re relying solely on savings and Social Security, the numbers might not add up.

Common Misconceptions That Could Cost You

❌ “I have Medicare, so I’m covered.” Nope—Medicare only pays for short-term stays in skilled nursing facilities under very specific conditions.

❌ “I won’t need long-term care.” Maybe not, but 7 out of 10 people over 65 will require some form of long-term care.

❌ “My family will take care of me.” While family support is invaluable, caregiving is physically and emotionally draining. Plus, your loved ones may not be able to provide the level of care you need.

How to Protect Your Retirement Savings

So, how do you keep long-term care from draining your hard-earned money? Start planning today. Here’s how:

1. Look Into Long-Term Care Insurance (LTCI)

LTCI helps cover the costs of care that Medicare won’t. The younger and healthier you are when you get it, the lower your premiums. Some policies even offer hybrid options that combine life insurance with long-term care benefits.

2. Consider a Health Savings Account (HSA)

If you have a high-deductible health plan, an HSA lets you save tax-free money for future healthcare expenses—including long-term care.

3. Use Your Pension Wisely

Some NC teachers take their pension as a lump sum, while others opt for monthly payments. Whichever you choose, make sure you’re strategically investing to stretch those dollars over your lifetime.

4. Set Up a Dedicated Savings Fund

A separate savings account just for healthcare expenses can give you extra security. Treat it like an emergency fund—because when it comes to long-term care, you never know when you’ll need it.

5. Explore Medicaid Planning

If you exhaust your resources, Medicaid may cover long-term care. But here’s the catch: You have to qualify financially. Proper planning (with the help of a financial advisor) can help protect some of your assets while ensuring you get the care you need.

FAQs About Long-Term Care Planning

Q: When should I start planning for long-term care?

A: The sooner, the better! Ideally, start in your 50s or early 60s while you’re still in good health and have more financial planning options.

Q: Is long-term care insurance worth it?

A: It depends. If you have significant assets you want to protect, yes. If you have very limited resources, Medicaid may be your best bet. A financial advisor can help determine the best path for you.

Q: What happens if I run out of money?

A: Medicaid can step in, but qualifying requires careful planning. Without proper strategies, you may have to spend down your assets before becoming eligible.

Final Thoughts: Take Control of Your Financial Future

Retirement should be a time of freedom, not financial stress. But if you don’t plan for long-term care, you could see your hard-earned savings vanish in a blink. North Carolina teachers—this is your wake-up call.

✅ Start planning now.

✅ Explore long-term care insurance.

✅ Make sure your savings strategy includes healthcare costs.

Want a personalized strategy to protect your savings? Let’s talk! Book a free 15-minute consultation, and let’s build a retirement plan that keeps your finances—and your future—secure. 🚀

📅 Ready to take the next step? Book your appointment today: https://bit.ly/4440F9l

💬 Have questions or want to dive deeper? Let’s connect!

💼 LinkedIn: https://www.linkedin.com/in/don-daves/

📘 Facebook: https://www.facebook.com/diamondadvisorgrp

YouTube: https://www.youtube.com/@diamondgroup4496/playlists

Subscribe To Our Weekly Resource Give Away

7 Essential Steps In

Planning Your Estate

May 18, 2022

9 Facts About

Retirement

May 12, 2022

What You Must Know 5 Years Before Retirement

May 04, 2022

4 Critical Social Security

Facts

April 27, 2022

The Pre-retirement

Checklist

April 20, 2022

Retirement Questions For Educators

April 13, 2022

How Tax Loopholes Will Lessen Your Tax Bills

April 06, 2022

2022 Annual Tax Guide

(How to Prepare for Tax Season)

March 30, 2022

Teachers' & State Employees' Retirement System Handbook

March 23, 2022

Blogs

Navigate the path to financial success with our blog! From savvy investment tips to practical budgeting advice, discover expert insights tailored for you. Secure your financial future with concise, actionable articles designed to empower your journey

Is Long-Term Care WIPING OUT Your Savings?

Is Long-Term Care WIPING OUT Your Savings?

What Every NC Teacher Needs to Know

Picture this: You’ve spent decades in the classroom, shaping young minds, grading endless stacks of papers, and finally—finally—you’re ready to retire. Your pension and savings should cover you, right? But then, an unexpected health issue pops up. A sudden need for long-term care, and before you know it, your nest egg is vanishing faster than you ever imagined.

This is the retirement nightmare that too many teachers face. The good news? You can take action NOW to protect your financial future. Let’s break down the real cost of long-term care and, more importantly, what you can do to keep your savings intact.

The Hidden Cost of Long-Term Care

Many people assume that Medicare will cover all their healthcare expenses in retirement. Spoiler alert: It won’t. Medicare provides only limited coverage for long-term care, leaving many retirees scrambling to pay for essential services like assisted living, nursing homes, or home health aides.

The Numbers Don’t Lie

Let’s talk real numbers. According to Genworth’s 2023 Cost of Care Survey, the average costs in North Carolina are:

In-home care: $4,900/month

Assisted living facility: $4,250/month

Nursing home (private room): $8,200/month

Multiply that by a few years, and you could be looking at a six-figure bill—and that’s without considering rising healthcare inflation!

Why NC Teachers Are Especially at Risk

North Carolina teachers have a solid pension, but let’s be honest—it’s not designed to cover massive healthcare expenses. Most teachers don’t have access to employer-sponsored retiree health benefits, and if you’re relying solely on savings and Social Security, the numbers might not add up.

Common Misconceptions That Could Cost You

❌ “I have Medicare, so I’m covered.” Nope—Medicare only pays for short-term stays in skilled nursing facilities under very specific conditions.

❌ “I won’t need long-term care.” Maybe not, but 7 out of 10 people over 65 will require some form of long-term care.

❌ “My family will take care of me.” While family support is invaluable, caregiving is physically and emotionally draining. Plus, your loved ones may not be able to provide the level of care you need.

How to Protect Your Retirement Savings

So, how do you keep long-term care from draining your hard-earned money? Start planning today. Here’s how:

1. Look Into Long-Term Care Insurance (LTCI)

LTCI helps cover the costs of care that Medicare won’t. The younger and healthier you are when you get it, the lower your premiums. Some policies even offer hybrid options that combine life insurance with long-term care benefits.

2. Consider a Health Savings Account (HSA)

If you have a high-deductible health plan, an HSA lets you save tax-free money for future healthcare expenses—including long-term care.

3. Use Your Pension Wisely

Some NC teachers take their pension as a lump sum, while others opt for monthly payments. Whichever you choose, make sure you’re strategically investing to stretch those dollars over your lifetime.

4. Set Up a Dedicated Savings Fund

A separate savings account just for healthcare expenses can give you extra security. Treat it like an emergency fund—because when it comes to long-term care, you never know when you’ll need it.

5. Explore Medicaid Planning

If you exhaust your resources, Medicaid may cover long-term care. But here’s the catch: You have to qualify financially. Proper planning (with the help of a financial advisor) can help protect some of your assets while ensuring you get the care you need.

FAQs About Long-Term Care Planning

Q: When should I start planning for long-term care?

A: The sooner, the better! Ideally, start in your 50s or early 60s while you’re still in good health and have more financial planning options.

Q: Is long-term care insurance worth it?

A: It depends. If you have significant assets you want to protect, yes. If you have very limited resources, Medicaid may be your best bet. A financial advisor can help determine the best path for you.

Q: What happens if I run out of money?

A: Medicaid can step in, but qualifying requires careful planning. Without proper strategies, you may have to spend down your assets before becoming eligible.

Final Thoughts: Take Control of Your Financial Future

Retirement should be a time of freedom, not financial stress. But if you don’t plan for long-term care, you could see your hard-earned savings vanish in a blink. North Carolina teachers—this is your wake-up call.

✅ Start planning now.

✅ Explore long-term care insurance.

✅ Make sure your savings strategy includes healthcare costs.

Want a personalized strategy to protect your savings? Let’s talk! Book a free 15-minute consultation, and let’s build a retirement plan that keeps your finances—and your future—secure. 🚀

📅 Ready to take the next step? Book your appointment today: https://bit.ly/4440F9l

💬 Have questions or want to dive deeper? Let’s connect!

💼 LinkedIn: https://www.linkedin.com/in/don-daves/

📘 Facebook: https://www.facebook.com/diamondadvisorgrp

YouTube: https://www.youtube.com/@diamondgroup4496/playlists

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Other Resources

Subscribe to our weekly resource give away. We create free resources about retirement, taxes, estate planning, debt pay-off, budgeting, college planning and other financial concepts that will help you in planning for your future.

Hear From Our Clients

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc risus, placerat non turpis eget, tincidunt tristique magna. Nunc id auctor nisi. Donec iaculis urna faucibus elit rhoncus interdum vel sed elit. Ut bibendum vestibulum sagittis.

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nunc elementum scelerisque felis vitae sagittis. Praesent vitae tincidunt sem. Vestibulum nunc

David Doe

Simple Company

© 2022 Diamond Advisor Group - All Rights Reserved

Disclaimer